OneGroup kicked off its 2024 101 Webinar Series on February 21st. OneGroup’s Medicare team, Shane Kelly and Connor Stanton spoke about the sometimes-confusing topic of Medicare, when you are eligible, what parts A, B, C, and D mean, when to sign up, and how to sign up.

When are you eligible?

You are first eligible for Medicare when you turn 65 years of age. You may also be eligible if you are under 65 but qualify because of a disability or other special situation. At 65 years of age, you become eligible for Medicare, regardless of whether you’re already receiving Social Security benefits or not. You also must be a United States citizen or legal resident and have lived in the United States for five consecutive years.

What do parts A, B, C, and D mean?

Medicare Part A – Hospital Coverage. Medicare Part A is provided through the United States government. It assists to cover inpatient hospital costs, short-term inpatient skilled nursing services, and Hospice care.

Most people do not pay a monthly premium for Part A if they or their legally married spouse have worked 40 consecutive quarters (ten years) and paid into the Medicare tax. Part A allows you to choose any qualified hospital in the United States that accepts Medicare, regardless of pre-existing conditions or medical history.

Hospital costs include a 2024 deductible of $1,632 for up to 60 days of inpatient care. Copayments increase after day 60.

If you have multiple hospital stays, each stay may require a separate deductible. For instance, if you pay a deductible during one admission and then return to the hospital three months later for an unrelated issue, you will need to pay another deductible for that subsequent stay.

Short term rehabilitative services in a skilled nursing facility require a three day hospital admittance before coverage begins. Services are covered for the first 20 days at no copayment cost per day, followed by a copayment of $204 per day from days 21 to 100.

With Medicare Part A, Hospice is always covered.

Medicare Part B – Medical Coverage. Medicare Part B is also provided through the United States government. Part B aids in the coverage of outpatient visit costs, including doctors’ visits, testing, medical services, and one-day surgeries. You can use Part B anywhere that accepts Medicare, but it generally does not cover care outside of the United States.

Similar to Part A, you cannot be turned away based on pre-existing conditions or health history. However, unlike Part A, Part B has a standard premium of $174.70 for the 2024 year.

Although there is a standard premium of $174.70 for 2024, you may be subject to a higher premium based on your 2022 income. Refer to the chart below for 2024 premiums based on 2022 income:

| If your yearly income in 2022 was: | You pay (in 2024) | |

| File individual tax return | File joint tax return | |

| $103,000 or less | $206,000 or less | $174.70 |

| $103,001 – $129,000 | $206,001 – $258,000 | $244.60 |

| $129,001 – $161,000 | $258,001 – $322,000 | $349.40 |

| $161,001 – $193,000 | $322,001 – $386,000 | $454.20 |

| $193,001 – $499,999 | $386,001 – $749,999 | $559.00 |

| above $500,000 | above $750,000 | $594.50 |

In addition to the standard premium, Medicare Part B has a deductible of $240 for the year 2024. Once this deductible is met, you can expect to pay 20% coinsurance for part B covered services, while Medicare covers the remaining 80%. An important note is that there is no out-of-pocket maximum for the 20% coinsurance, meaning there is no limit on how much you may have to pay for the 20% coinsurance.

Medicare Part C – Medicare Advantage. Medicare Advantage is a single plan offered by private insurance companies that combines coverage from Medicare Part A, Part B, and often Part D (prescription drug coverage).

Medicare Advantage plans can often offer additional benefits such as dental, vision, hearing, and some preventative care that are not covered by original Medicare.

Although you still must be enrolled in Part A and B, when enrolled in a Medicare Advantage plan the insurance carrier becomes your primary payer instead of the United States government.

Medicare Advantage plans use a network of healthcare providers typically through a health maintenance organization (HMO) or a preferred provider organization (PPO). With an HMO, you must use in-network providers. With a PPO, if your doctor approves the insurance carrier, you are able to see both in-network and out-of-network healthcare providers with a possible small increase in copayment amounts.

Other advantages of a Medicare Advantage plan include $0 premium in most areas, maximum out-of-pocket limits, and controlled spending on hospital and medical coverage.

Medicare Part D – Prescription Drugs. Medicare Part D assists with the cost of prescription drugs offered through private companies. Similar to Part C, Medicare Part D is offered through private insurance carriers that follow Medicare guidelines. Each plan has a drug coverage list that can vary by carrier and year.

Similar to Part B, Part D has a monthly premium calculated by your 2022 income. Refer to the chart below for 2024 premiums based on 2022 income:

| If your yearly income in 2022 was: | You pay (in 2024) | |

| File individual tax return | File joint tax return | |

| $103,000 or less | $206,000 or less | $0.00 |

| $103,001 – $129,000 | $206,001 – $258,000 | $12.90 |

| $129,001 – $161,000 | $258,001 – $322,000 | $33.30 |

| $161,001 – $193,000 | $322,001 – $386,000 | $53.80 |

| $193,001 – $499,999 | $386,001 – $749,999 | $74.20 |

| above $500,000 | above $750,000 | $81.00 |

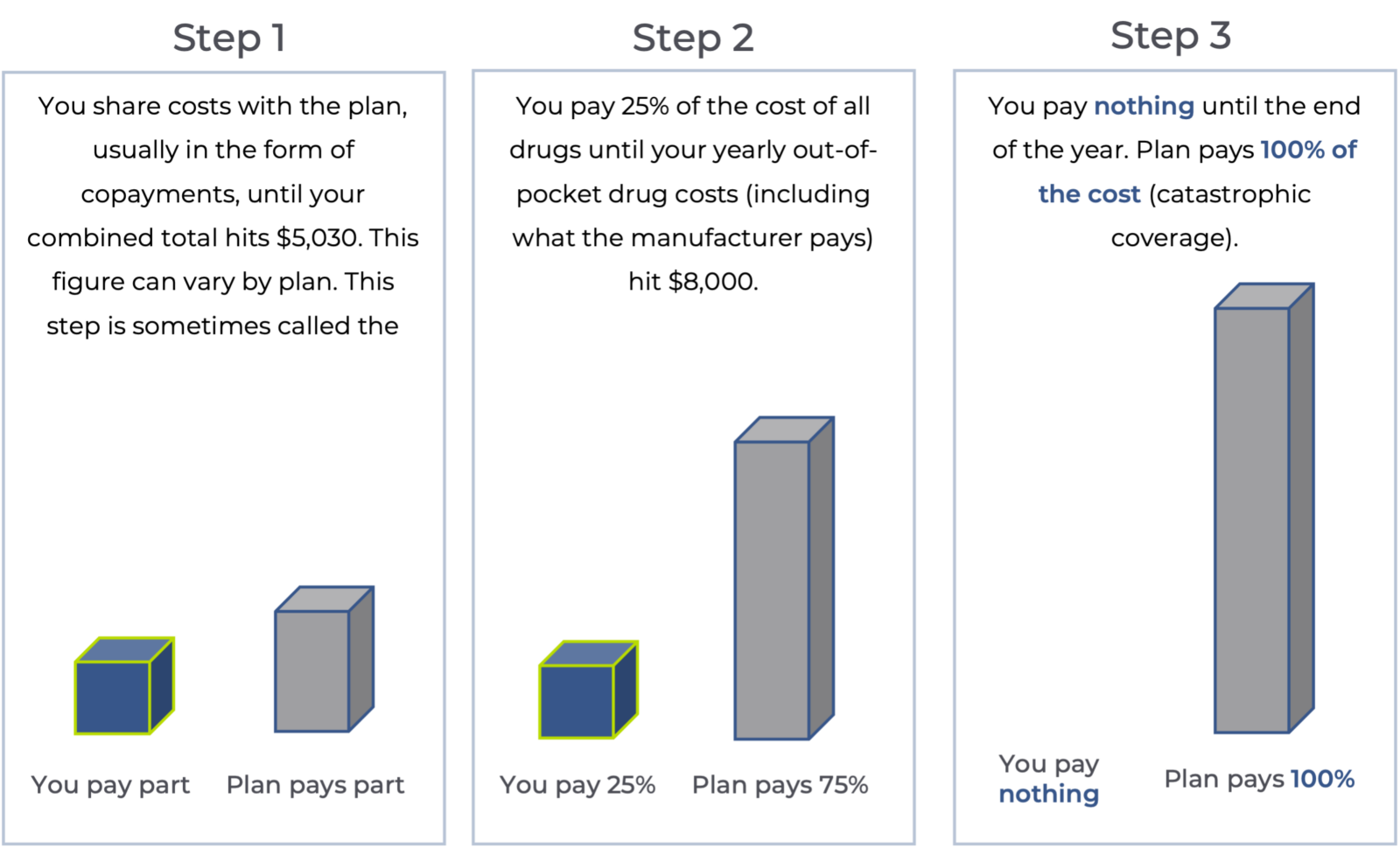

Medicare Part D also includes what is known as cost sharing. Below outlines where cost sharing is applicable to you and at what dollar amount.

Please note – due to the Inflation Reduction Act beginning in the year 2024, cost sharing for Part D drugs will be eliminated for beneficiaries in the catastrophic phase of coverage.

When and how to enroll?

Automatic enrollment. You will be automatically enrolled in Medicare Part A if you are already collecting Social Security. You cannot opt out of Part A since you will no longer be HSA eligible. However, you can opt out of Part B with some applicable considerations.

Enrollment process. If you are not collecting Social Security, you must go through the enrollment process for Medicare Part A and Part B. To enroll directly, you can do so;

Online: at Medicare.gov or SSA.gov/benefits

By phone: 1-800-772-1223

In-person (appointment required): Your local Social Security office.

As a reminder, if you are receiving Social Security, you will automatically be enrolled in Medicare Part A and B.

When am I covered? Coverage is effective the first day of the month that you turn 65. If your birthday lands on the first of the month, coverage will start the month prior. For example, if your birthday is October 20, your coverage will begin October 1. If your birthday is October 1, your coverage will begin September 1.

If you enroll in coverage after the age of 65, coverage will be effective the first of the following month. If you choose to elect coverage after you turn 65, you will be in a special enrollment period.

When to enroll. When you turn 65, you must enroll in Medicare Part A, B, and D to avoid late enrollment penalties (unless you qualify for an exception or still have credible coverage and can delay enrollment.) You have a seven-month window that is known as your initial enrollment period. This period consists of three months before your 65th birthday, your 65th birthday month, and three months after your 65th birthday month.

Although you have ample time to enroll in Medicare, if you enroll after the initial enrollment period, premiums could be higher, again, unless you qualify for an exception or still have credible coverage.

Medicare late enrollment penalties. Although you may opt out of Part B if you’re eligible to, if you do not enroll in Part B until after your initial enrollment period, premiums will increase 10% ($174.70) in 2024 for each 12 months until you do enroll.

For Part D, a late enrollment penalty applies if you go without prescription drug coverage for 63 or more consecutive days after your initial enrollment period. The Part D late enrollment penalty is calculated by multiplying one percent of the “national base beneficiary premium” (34.70 in 2024) by the number of full, uncovered months you were eligible but didn’t join a Medicare prescription drug plan and went without other credible prescription drug coverage.

If you continue to work after 65, you have options. If you continue to work and have credible coverage, you are not required to enroll in Medicare as soon as you turn 65. There are a few other options that you may want to consider.

You can stay on your current plan and delay enrollment in Medicare if you or your legally married spouse’s plan counts as credible coverage. Credible coverage is considered a plan at a company with more than 20 full time employees.

You also can leave your current plan and enroll into Medicare as well as add an Advantage, Supplement, or Part D prescription drug plan.

If you decide to continue your company’s plan, you will be able to enroll in Medicare when you retire or when you are no longer receiving credible coverage.

What if I have a special situation?

Medicare can be very specific to each recipient and the overarching “rules” may not apply to your situation. We recommend reaching out to a licensed Medicare professional to answer more specific questions about your situation and which Medicare option may be best for you!

Additional thoughts regarding Medicare coverage

Medicare Supplement Insurance Plans or Medigap Plans. An alternative option in addition to Medicare Parts A through D is a Medicare Supplement or Medigap plan. These plans aid in paying a portion of the costs associated with Medicare Parts A and B and are available through private insurance carriers. These types of plans cover some or all out-of-pocket expenses under Part A and Part B.

If you enroll in a supplement plan, Medicare Part A and Part B still act as your primary payer. The supplement plan then becomes secondary but still covers certain costs of Medicare Part A and B depending on the specific plan. There are no network restrictions and no referrals required.

The set monthly premium for these plans varies depending on the levels of coverage.

COBRA. If you are over 65, COBRA is not a viable coverage option. If you retire before you are 65 and elect COBRA to bridge the gap until Medicare, turning 65 will be a qualifying event for you to come off COBRA and enroll in Medicare. Verify with your employer how long COBRA will be provided, as different employers have varying time limits on COBRA.

Health Savings Accounts. Once you enroll in any form of Medicare, you are no longer allowed to contribute to a Health Savings Account (HSA). However, you may continue to use the money you have already accumulated in your HSA for eligible expenses. These eligible expenses include, Qualified Medical Expenses (QME), premiums for long-term care insurance, and premiums for individuals over 65 such as retirement health benefits and Medicare premiums.

Once you reach 65, you may also take a distribution for a non- medical expense and pay regular income tax on the contributions. Similar to taking a distribution from a 401(k) or an IRA.

If you continue to work past the age of 65, you should stop contributing to your HSA six months prior to the election of Social Security benefits to avoid penalties.

Contact us and OneGroup’s next 101 Webinar.

Everyone’s needs regarding Medicare are different. If you have questions regarding this webinar or your Medicare options please contact Shane Kelly or Connor Stanton via the information below, or submit a form here and mention this webinar to be connected to a OneGroup Medicare expert. OneGroup offers its Medicare services free of charge.

Shane Kelly, Medicare Team Lead

P: 680-207-6873

Connor Stanton, Licensed Specialist

P: 680-207-6874

OneGroup is looking forward to the next webinar in the series, Human Resources 101, on Wednesday, April 17, 2024 from 9:30 AM – 10:30 AM EST. Human Resources Consulting Manager, Colleen Williams and Human Resource Consultant, Travis Simpson will discuss best practices to avoid costly employment claims. Register for OneGroup’s next webinar here.

Standard disclosure: We are not a government agency. We are licensed insurance agents who discuss insurance programs such as Medicare Advantage, Medigap, and Medicare Part D Prescription Drug Coverage. Any information we provide is limited to those plans we do offer in your area. Please contact Medicare.gov or 1-800-Medicare to get information on all of your options.

This content is for informational purposes only and not for the purpose of providing professional, financial, medical or legal advice. You should contact your licensed professional to obtain advice with respect to any particular issue or problem. Please refer to your policy contract for any specific information or questions on applicability of coverage.

Please note coverage can not be bound or a claim reported without written acknowledgment from a OneGroup Representative.